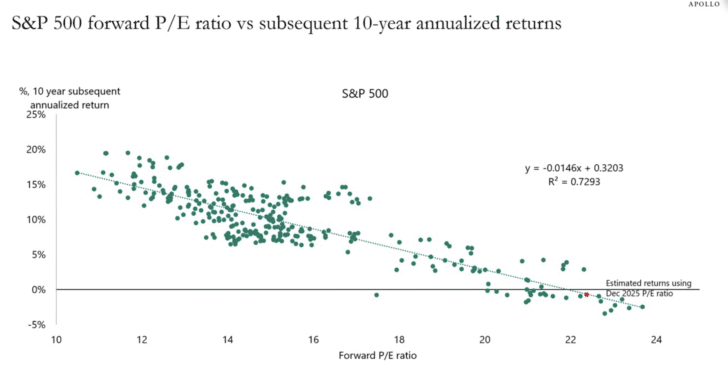

Beyond expensive valuations, with the S&P 500 trading at roughly 22 times estimated forward earnings, another concern for the stock market is quietly flashing red: U.S. households now have more net worth in stocks than in real estate.

On the surface, this might not sound alarming. After all, the stock market has been ripping higher since 2020, aside from 2022. Stocks have dramatically outperformed real estate over the past several years, especially after the Federal Reserve began hiking interest rates aggressively. However, I argue housing affordability has improved as a result of the bull market in stocks. Just look at your own stock portfolio.

When one asset class performs better for longer, people allocate more capital to it, whether consciously or not. Retirement accounts grow. Brokerage accounts swell. Equity compensation vests. Real estate, by contrast, is illiquid, capital intensive, and much less exciting during periods of high interest rates.

That said, I now find commercial real estate attractive relative to stocks, which is why I am slowly dollar cost averaging into private real estate opportunities. When sentiment is poor and capital is scarce, expected future returns tend to be higher. That is rarely the case when everyone is euphoric.

Concentration Risk Risng

When households hold more of their net worth in stocks than in real estate, we should pause. Concentration risk matters. The higher the concentration in one asset class, the more fragile sentiment becomes if prices start to fall. It sure feels like 1999 is returning.

With more capital tied to stocks, any meaningful correction has the potential to feel more violent. Losses hit closer to home. People check their balances more often. Panic selling becomes more likely, not because fundamentals suddenly collapsed, but because fear spreads faster when there is more at stake.

Capital flows matter. When there is more money in stocks, there is also more money that can be sold. This dynamic tends to amplify market moves on the downside, especially when leverage, margin debt, and passive investment vehicles are involved.

Compared to selling real estate, selling stocks is cheap and almost instant.

The Ominous Signal for Stocks

If you look at historical data, the last two periods when households owned more stocks than real estate were followed by prolonged periods of disappointment for equity investors.

In the 1970s, stocks stagnated in real terms as inflation eroded purchasing power. In the late 1990s and early 2000s, households became heavily overweight equities following the tech bubble. What followed was a “lost decade” for stocks from 2000 through roughly 2012, during which the S&P 500 delivered essentially zero real returns.

History does not repeat perfectly, but it does rhyme often enough to deserve respect.

Chasing Performance Is Human Nature

It is human nature to chase what has been working. Nobody wants to miss out, especially after watching others get rich seemingly effortlessly. Stocks are liquid, easy, and rewarding during bull markets. Real estate feels slow, annoying, and burdened with tenants, repairs, and taxes.

But this is exactly when discipline matters most – when investing FOMO is at its highest. Make sure you are properly diversified based on your risk appetite.

When an asset class dominates household net worth, future returns tend to be lower, not higher. Expectations rise. Margins of safety shrink. At the same time, diversification quietly erodes as portfolios drift toward what has already gone up the most.

This does not mean stocks are about to crash tomorrow. But nobody should be surprised if they do.

I am tempering expectations and resisting the urge to aggressively chase upside at these levels. I am also deliberately allocating new capital toward areas that feel less crowded, including private real estate, credit, and select alternatives.

Why Real Estate Still Matters

Real estate remains a core store of wealth for households for a reason. It provides shelter, income, inflation protection, and psychological stability. Even when prices stagnate, people still live in their homes. Rents still get paid. Mortgages still amortize.

Stocks, by contrast, provide no direct utility. They are pure financial assets whose value depends on earnings expectations, liquidity, and sentiment. When sentiment turns, prices can fall far faster than fundamentals justify.

This is why having balance matters. When too much wealth is tied to assets that can reprice instantly, emotional decision making becomes more dangerous.

Historical Correction Frequency In Stocks

Given current valuations and household exposure, I would not be surprised to see another 10 percent or greater correction in the next 12 months. All it takes is one catalyst. A growth scare. A policy mistake. A geopolitical shock. A liquidity event.

Corrections are not abnormal. They are the price of long term returns. But when concentration is high, corrections feel worse than expected. To put declines into perspective, here’s how often they happen:

- 5% pullbacks: 2-3 times per year

- 10% corrections: ~every 1-2 years

- 20% bear markets: ~every 5-7 years

- Recessions: every 7-10 years

The solution is not fear. The solution is preparation.

Rebalance when necessary. Diversify intentionally. Build assets that provide cash flow and utility, not just paper gains. And remember that when everyone feels comfortable, risk is usually higher than it appears.

Stocks may continue higher in the short term. But when households already have more wealth in stocks than in real estate, it pays to be a little more careful than the crowd.

Readers, what are your thoughts on Americans now holding more wealth in stocks than in real estate? Do you see this as a warning sign for stocks, an opportunity to buy real estate, or both? And roughly what percentage of your net worth is allocated to stocks versus real estate today?

Diversify Your Wealth Beyond Public Stocks

If households already have more of their net worth in stocks than in real estate, it’s worth asking a simple question: What happens if public equities finally mean revert? Concentration risk tends to feel invisible during long bull markets, until it doesn’t.

For those who don’t want the headaches of owning and managing physical property, I’ve found Fundrise to be a compelling alternative. The platform allows investors to passively invest in diversified portfolios of residential and industrial real estate, with a focus on Sunbelt markets where valuations are generally lower and long-term demographic trends remain favorable.

With more than $3 billion in private assets under management, Fundrise provides exposure to real estate that behaves differently than public REITs and stock-heavy portfolios—something I increasingly value as households tilt further toward equities.

I’ve personally invested over $400,000 with Fundrise. They’ve been a long-time partner of Financial Samurai, and with a $10 minimum investment, it’s one of the easiest ways to start diversifying beyond traditional stocks and bonds

If you want ongoing insights about asset allocation, valuation risk, and building wealth with less stress, join over 60,000 readers and subscribe to my free newsletter. Since 2009, I’ve shared firsthand experiences to help readers grow wealth, gain financial independence, and sleep better at night, no matter where we are in the market cycle.

Read the full article here