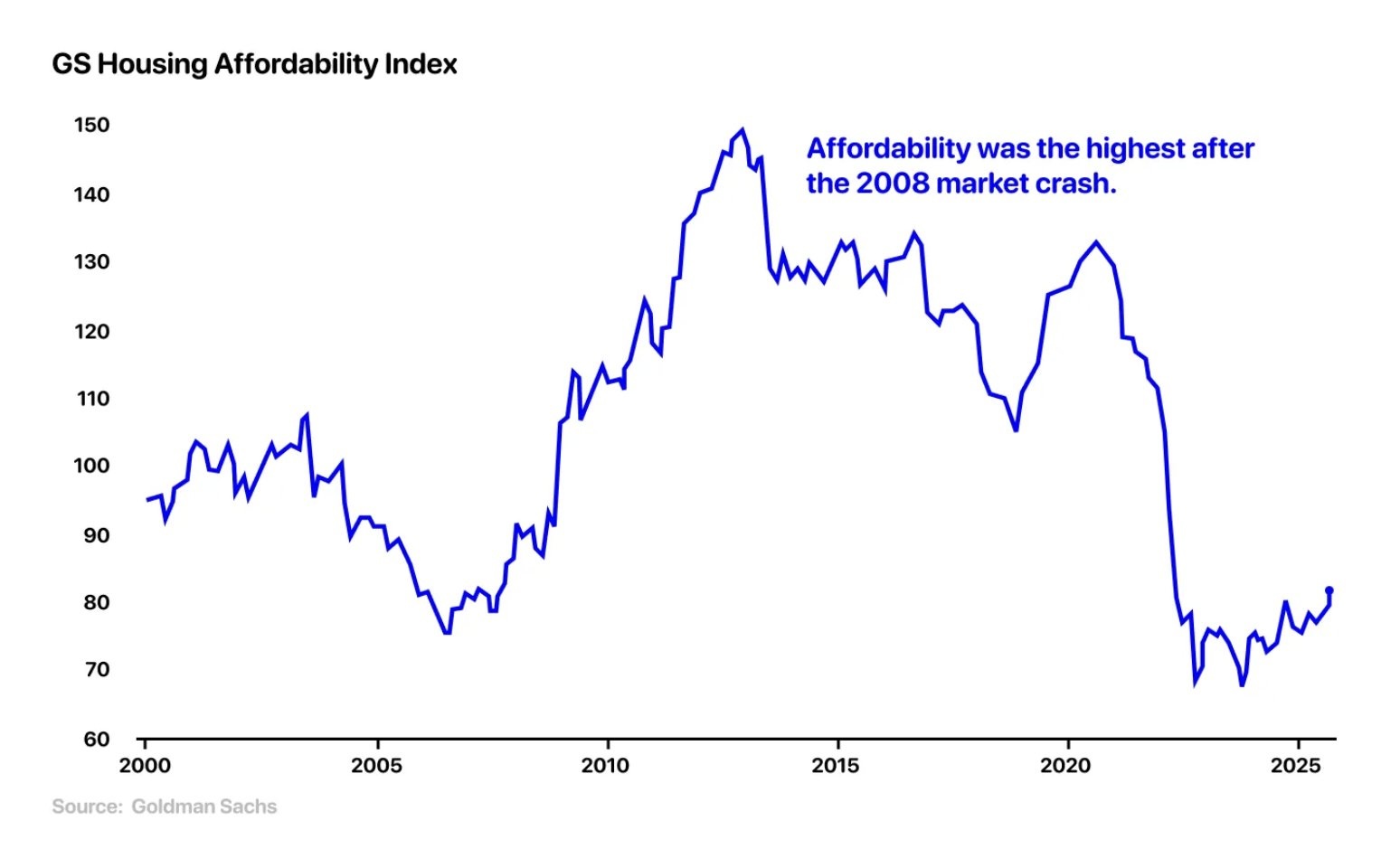

Conventional wisdom says we’re in a housing affordability crisis. With higher mortgage rates and higher home prices, buying a home has supposedly never been more expensive. But what if I told you this entire narrative might be wrong? In reality, housing affordability could actually be at or near an all-time high.

Sound crazy? Maybe. But if housing were truly so unaffordable, why haven’t prices crashed? It would take a 38% decline in home prices (could happen) or a 60% surge in household incomes (highly unlikely) just to claw back to 2019 affordability levels. The widest gap in history.

Yet, why do prices in many markets continue to stay flat or march higher? Yes, the lock-in effect from pandemic-era refinancing plays a role. And yes, there’s a national undersupply of homes. But those can’t be the only explanations, especially if affordability is as catastrophic as the data claim.

At Financial Samurai, we’re financial practitioners who connect the dots through firsthand experience. It’s entirely possible that politicians, economists, and real estate think tanks have the concept of “housing affordability” completely backwards.

Housing May Be More Affordable Than Everyone Realizes

With higher mortgage rates and higher home prices, the usual solutions offered to lower housing costs are: pressure the Federal Reserve to cut rates (which doesn’t even control mortgage rates), push for 50-year mortgages to lower monthly payments, or create more incentives to build new housing. Long term, yes, increasing supply is the best way to lower rents and home prices.

The thing is, maybe none of these suggestions are necessary at all. What if, thanks to massive stock market gains and rapidly appreciating private company equity, housing affordability is actually higher today than ever?

If you examine where most wealth has been created since 2020, let alone 2012, the answer becomes pretty obvious: a bull market in equities has massively outpaced the rise in home prices, thereby increasing housing affordability for those who participate in wealth-building assets.

Why A Bull Market In Stocks Makes Housing More Affordable

The #1 thing anti-homeownership advocates say is that it’s “cheaper to rent than own.” The argument goes: renters can save and invest the difference, and if they simply invested diligently in the S&P 500, they’d be wealthier.

Even though I believe the average American can build more wealth in real estate than investing in their 401(k), let’s take the “save and invest the difference” mantra at face value.

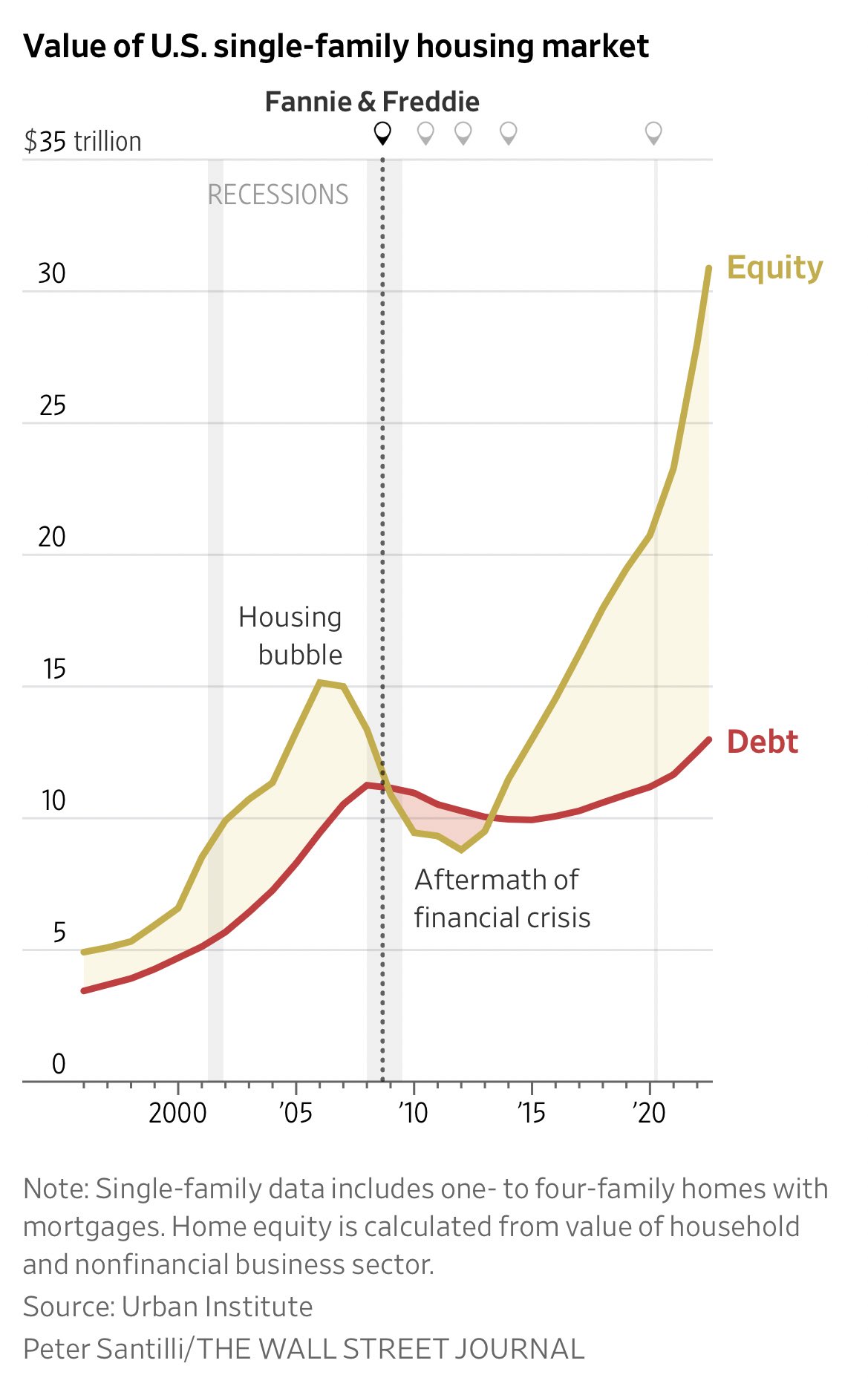

From January 1, 2020 through December 1, 2025, the S&P 500 is up roughly 115% including dividends. Over the same period, the median U.S. home price only increased by ~50%, rising from ~$267,000 to ~$410,000.

If your stock investments double while home prices go up only half as much, housing has actually become more affordable using the same amount of invested capital. Over the past decade, stocks have beaten housing by roughly 65 percentage points.

This comparison assumes you invested an amount equal to a home’s purchase price into stocks. But since most first-time homebuyers only put down 20% or less, rising stock market wealth has made it even easier to afford a home. After all, we are assuming that renters are diligently saving and investing the difference.

Let me give you three real-life examples.

Example #1: A House Became Affordable Only When Stocks Rebounded

In 2022, I wanted to buy my house but couldn’t afford the asking price. I wanted to pay all cash because I was tired of having a mortgage, rates were high, and I could get a better deal. The S&P 500 fell about 18%, and because my portfolio was tech-heavy, I was down closer to 26%. Ouch. Higher volatility is the price you pay for investing in growth stocks.

Then stocks rebounded sharply in 2023, and the house came back on the market at a lower price.

The combination of higher stock prices and a lower house price made the home affordable. Without the stock market rally, the house would have still remained out of reach.

Had we waited until late 2025, the house would’ve been even more affordable for us from a stock-gain perspective, since equities rose another ~60% between 2023 and 2025. But that assumes the home didn’t appreciate further from its 2003 baseline (it did by perhaps 15% – 25%), and assumes it would still be available (highly unlikely given the rarity of the large lot size).

If stocks didn’t go up since I left traditional work in 2012, I wouldn’t have been able to climb the property latter. I simply didn’t have a significant and steady active income stream to help me come up with larger down payments.

Example #2: My New Tenants Just Got 3 Years Of “Free Rent” Thanks to Company Stock

I recently found new tenants for my renovated 5-bedroom, 4-bathroom San Francisco home. The previous tenants, a family of four, paid $9,200 per month. Given surprising demand for another rental I’d leased earlier, I tested the market at $10,000 per month.

It took about three weeks, but I found tenants who were a couple, not a family. One works at a private tech company. The other works for one of the most popular AI companies today, which was valued at $185 billion in September 2025.

Based on their base salaries alone, $10,000/month rent was less than 20% of their gross income. Paying less than 30% of your gross income to rent or a mortgage is considered affordable.

But here’s the kicker: about 2.5 months after his company’s $185B valuation, it raised $15 billion more at a $350 billion valuation. Based on his seniority, I estimate he received around $500,000 in equity vesting over four years, which by now is worth closer to $1 million.

If his $500,000 gain in stock value translates to roughly $360,000 after taxes, then:

His stock appreciation alone could pay their rent for 36 months.

That’s three years of “free” living in a 5-bedroom ocean-view home in San Francisco, courtesy of his company’s rising valuation.

If “free” isn’t housing affordability, what is? If they want to buy a home in the future, it would certainly be more affordable given their company equity is growing far faster than the growth rate of San Francisco home prices.

The Missing Variable: Stock Gains in Housing Affordability Calculations

Economists and politicians talk endlessly about the following variables for stock market affordability:

- income

- home prices

- rent prices

- mortgage rates

- property taxes

- insurance rates

But they ignore two huge forces:

- Public and private stock gains, which dramatically enhance purchasing power

- The Bank of Mom & Dad, which provides down payments for a growing percentage of homebuyers

This article focuses on the first, even though we know there are trillions of dollars set to be inherited from the Boomer generation.

Example #3: Google Gaining Another Trillion In Market Cap

Forget about me and my tenants. Consider the roughly 35,000 Google employees in the Bay Area. Google stock has surged by more than 65% in 2025. If 30% of a typical tech worker’s compensation comes from equity, then their total comp effectively rose 20%.

A Googler making $280K salary + $120K stock goes from:

$400K total comp to -> $478K total comp.

They feel richer and they are richer.

And their existing unvested stock grants, which might have been worth $360,000 at the beginning of the year, are now worth 65% more to $594,000 as well.

Bay Area housing isn’t becoming affordable because prices are falling. It’s becoming more affordable because the people who buy the homes are getting wealthier far faster than prices are rising.

The NASDAQ vs. San Francisco Housing

Now let’s forget Google, and look at the NASDAQ. It is up about 160% since January 1, 2020.

Meanwhile, the median San Francisco home is up 15–40%, depending on price point and property type.

That means the typical tech worker or NASDAQ investor also finds housing affordability increasing, not decreasing.

And remember: most buyers don’t pay cash.

A $2.5 million home in 2020 that’s now worth $3 million requires a down payment increase of only:

$500,000 -> $600,000.

That extra $100,000 is easily digestible for a household making $400,000 – $600,000 a year and living off $180,000 – $300,000 gross. They are already saving over $150,000 in cash a year. So thanks to increased affordability five years later, they could look at a $3.5 million house with a $700,000 down payment or greater instead.

Housing affordability is not just about mortgage rates. It’s about asset appreciation relative to housing appreciation.

Housing Affordability Continues To Increase As Stocks Rise

The dominant narrative is that housing is unaffordable. But if you look at where wealth has actually been created since 2020, the reality flips:

- Stocks have massively outperformed housing.

- Tech workers’ compensation packages have increased partly because their company’s stock has increased

- Investment bankers are receiving record bonuses.

- Parents are increasingly funding down payments.

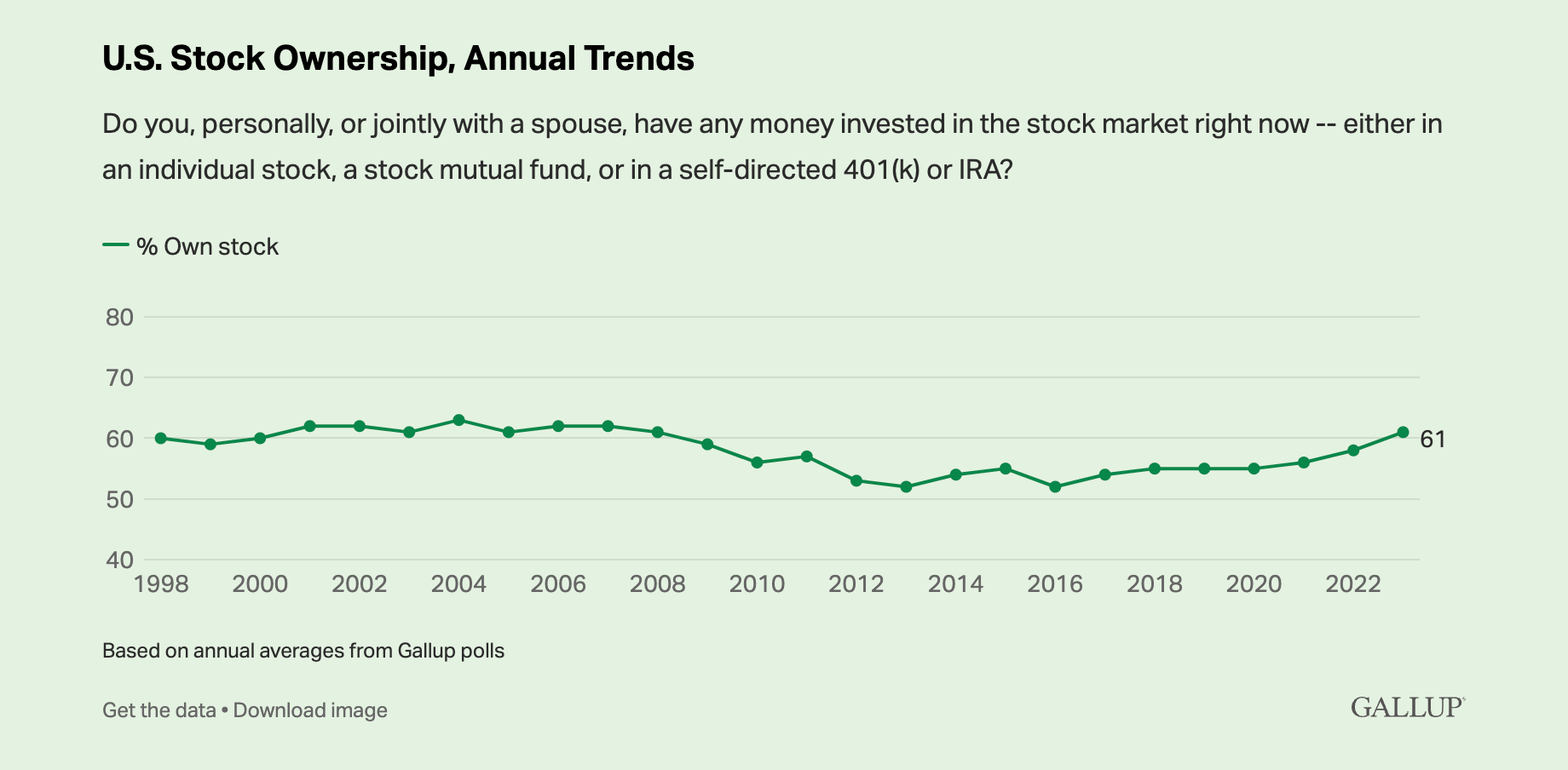

- Roughly 63% of all Americans own stocks

Housing affordability is only a crisis for those who don’t own appreciating assets. Thankfully, for the majority of Americans, the bull market has quietly made buying (or renting) a home easier, not harder.

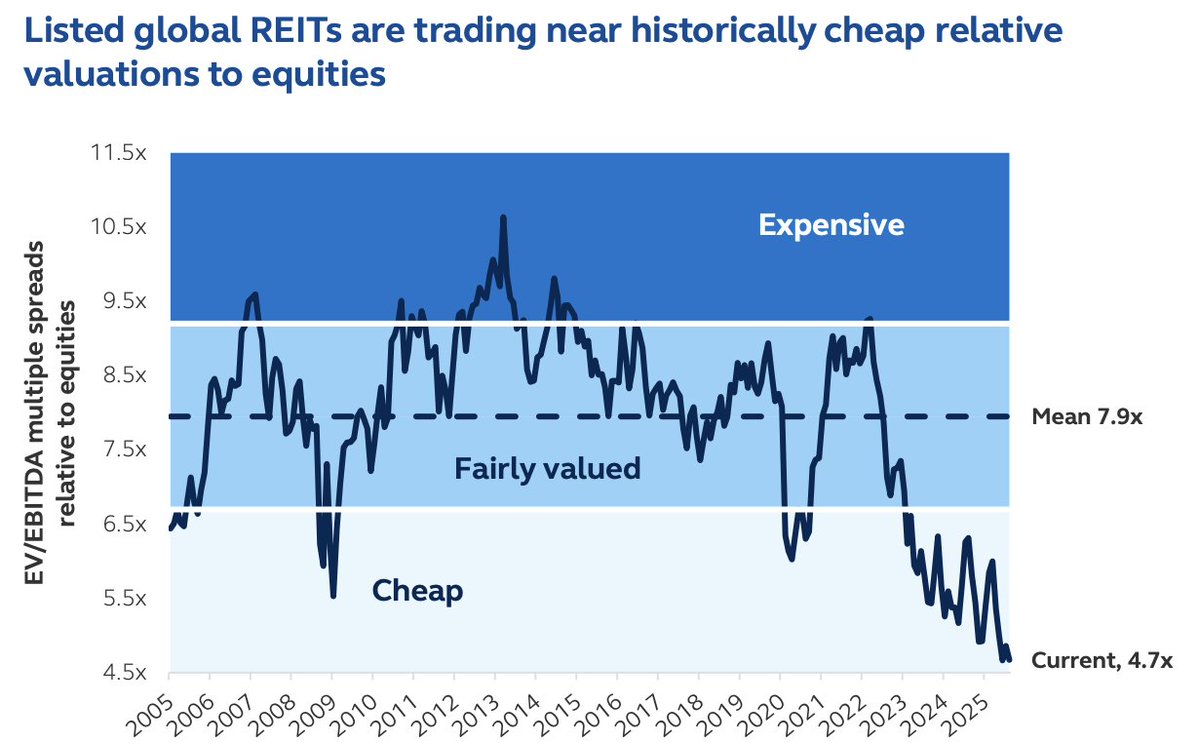

This chart perfectly illustrates my point from an investors point of view. Global REITs and commercial real estate are at historically cheap valuation levels compared to equities, which is why I’m investing in commercial real estate today.

The Solution to Improving Housing Affordability

The most effective long-term solution to improving housing affordability for all is to expand broad ownership of American companies through stock ownership.

The government should promote better personal finance education and offer stronger incentives for investing, both for adults and their children. When kids start investing early, they naturally develop an ownership mindset. They gain skin in the game and become more motivated to work, save, and build their future.

Obviously, we still have a long way to go to improve housing affordability for everyone, not just the 63% of Americans who own stocks, or people working in highly paid professions. I’m doing my part by writing three posts a week and a weekly newsletter for free since July 2009. I also wrote my latest USA TODAY national bestseller, Millionaire Milestones, to help more people build wealth. But there’s so much more we can all do.

The more we grow our wealth through stocks, the easier it becomes to afford not just a home, but everything else life throws our way.

Readers, is the narrative about a housing affordability crisis wrong? Do you think housing has actually become more affordable thanks to stock market gains over the years? If all renters were diligently saving and investing the difference, how could the cost of living really be worse given the bull market?

Invest In Real Estate Without A Big Down Payment

If you see the compelling relative value in commercial real estate compared to equities, take a look at Fundrise, my preferred private real estate investment platform. Fundrise focuses on acquiring and building residential and industrial properties in lower-cost, higher-yield markets across the country. It’s a simple way to diversify beyond stocks and tap into institutional-quality real estate opportunities.

With an investment minimum of only $10, it’s easy to dollar-cost average in and gain exposure. Fundrise is a long-time sponsor of Financial Samurai and Financial Samurai is a multiple six-figure investor in Fundrise products.

Read the full article here